We continue publication of Yegor Vlasenko’s paper «The Retreat of the State: Liberalisation of the Housing Market in Ukraine». This publication has been prepared during the Master’s program in Urban Studies at the University of Malmö through the Swedish Institute (SI) scholarships.

All prominent housing researchers inform us on the alarming situation with housing in the world and predict growing homelessness, too high rents for the upcoming generations, and further socio-spatial segregation in cities. What does all of this have to deal with subprime mortgage crisis in the US and neoliberal housing policy? Will these pessimistic forecasts affect Ukraine? How can housing prices dynamics be explained, and who can influence it? Some facts and thoughts on this are to be further presented in the third part of the article about the retreat of state from the housing market in Ukraine.

With entrance of global finance to housing market through mortgages and their securitization, housing has become a backbone of many national economies, as well as an integral element of the global financial system. Sustained price appreciation for almost a decade in 1990s — early 2000s turned housing into a major source of wealth (Smith & Searle, 2008), with excessive wealth generated through mortgage equity withdrawal (MEW) channelling into consumption (Ong et al., 2013). Surely, the growing role of housing market was directly connected with retreat of state and its social welfare model from housing in many countries in 1980s, in line with the overall market liberalization, most often associated globally with Reaganism and Thatcherism (Smith, 2014). In this respect, housing privatisation in Ukraine should be rightfully linked to this global movement that affected economic and social policy of the Soviet Union during perestroika reforms and triggered market liberalization, which continued in independent states of post-USSR. However, as pointed out by Sager (2011), privatisation and commodification of housing are essentially different things, although are obviously interconnected.

In order to reap the market benefits from privatisation, passing the housing stock to private owners appears to be not enough (Sager, 2011), as proved by Stakhanov case mentioned earlier. Typically, establishment of a liquid housing market requires new credit institutions aimed to serve and regulate the new housing markets. As vividly shown by pre-2008 global financial crisis period, further financial liberalization affecting operation of credit institutions related to housing that followed overall market growth created a ‘perfect storm’ of owner occupation purchases (Smith, 2011), when housing markets were liquid, mortgages flexible, credit cheap and in good supply and regulatory regimes relaxed (Ong et al., 2013).

It is important to highlight the nature of these new housing markets. Unlikely to traditional neoclassical approaches that helped to explain home price dynamics in the past, the new markets seem to lack the ‘rational economic person’ as a key actor (Smith, 2011), opening such basic terms as supply, demand, competition, price and value to scrutiny (Smith, Munro & Christie, 2005). Instead, almost full commodification and marketization of urban housing is believed to be governed by the rules of neoliberal market system (Sager, 2011), often ironically (and sometimes seriously) mentioned in literature as ‘the villain of the XXI century’ (Smith, 2014). The externalities of this system exposed by the global financial crisis in 2008 proved that markets are no longer abstract economic concepts, since they are linked to value-laden human activities, moralities and sensibilities (Smith, 2014). This affects values on these markets, making them deeply institutionalized rather than set by an open market competition.

What are the key feature of neoliberal housing markets then? Firstly, neoliberal ideology tends to prioritise the economic aspects of housing over the social aspects, which puts social housing under pressure, along with the model of European welfare state. This also includes transfer of decision-making on housing maintenance and rehabilitation to the private sector, which implies allocation of resources to these tasks in accordance with market criteria.

Secondly, neoliberal transformation of cities triggers gentrification, most broadly defined by Sager as ‘a process involving a change in the population of land-users such that new users are of a higher socio-economic status that the previous users’, but most commonly known as the new colonization of cities by the middle classes, who often represent global elite group of professionals described by Florida (2005) as ‘the creative class’. Particularly, gentrification is linked to neoliberal urban regeneration, for example revitalization of downtowns of North American cities, once abandoned by the middle class. A single most important externality of gentrification is displacement of tenured residents and whole local communities through rent increases and inability to secure another dwelling in a certain neighbourhood.

Thirdly, neoliberal city re-creates quite obsolete spatial dimension of social stratification through putting physical barriers separating residents within a certain neighbourhood. The rise of gated communities, inhabited by a homogeneous social group, embrace segregation and create false sense of security, in reality provoking much faster marginalization and stigmatisation of neighbourhoods located ‘on the wrong side of the fence’. It is important that these practices of social exclusion are often not recognized as such (Sager, 2011), since public opinion is concentrated rather on lifestyle advantages of such communities, than on their design that prevents social contacts. Finally, this type of community results in privatisation of public space, somehow dismantling positive effects of liveable streets and neighbourhoods described by Jane Jacobs.

While liberalization implication in housing policy concerning privatisation in Ukraine is quite obvious, it is important to further study dynamics of the local housing market in 2000s before, during and after the global financial crisis, which certainly had a significant impact on economic situation in Ukraine. After severe economic crisis and several waves of hryvnya devaluation in 1990s, macroeconomic situation more or less stabilized, allowing economic growth and increased consumption thanks to slow yet steady income increase. This period of economic recovery and rapid growth of consumer goods and services industry was also noticed by international banking institutions, many of which made a decision to enter the Ukrainian market, offering various financial services, including mortgage finance.

Additionally, economic recovery allowed overcoming apathy of real estate markets and starting commercial housing construction in key cities, such as Kyiv, Odesa, Dnipropetrovsk and Kharkiv. These new construction forms and private developers successfully abandoned dependence on state-funded housing projects and quickly learnt how to work with individual investors and financial institutions, offering various housing projects, which seemed much superior to Soviet-era construction. This emerged industry recognized a need that existed both in qualitative and quantitative dimension. As mentioned, after decades of socialist modernist housing construction many citizens became tired of monotonous gray concrete panel housing based on very modest regulations on living standards. On the other hand, an already existing in 1990s housing shortage became very visible by early 2000s. In 2003 the average number for apartment space per person in Ukraine was 21.6 sq. meters, compared to 40.5 sq. meters in Germany (Giucci et al., 2007). Hence, purchase of new housing through mortgage finance scheme became quite common and popular, while interest rates remained relatively low.

The re-emergence of the housing market effectively capitalized the privatized housing stock, proving it to be extremely good investment, especially in big cities. While large-scale public and private rental market never came to existence, a vast black market for apartment rental emerged quite swiftly, enjoying absence of regulations or simply ignoring them. Renting an apartment without a contract, insurance and, subsequently, paying taxes became a common practice, make rental housing a seller’s market and putting tenants into extremely vulnerable position. However, sunk costs of initial socialist housing construction and free privatization allowed to put rents in an environment extremely close to textbook supply and demand economy, using a preference of location as a key criterion for market competition. It is also necessary to mention that rental market used to be part of a shadow, unofficial economy back in the Soviet times, which left a behavioural pattern that is extremely hard to overcome.

The emergence of an obviously profitable housing market triggered another important development, which is still a key feature of Ukrainian economy — housing had become the most popular haven for excessive financial capital investment. While bank deposits rates stayed at a low level, especially in comparison to loan interest (Giucci et al., 2007), internal stock market remained too fragile and unpredictable and investment into foreign property and securities remained under heavy fiscal regulation, housing proved to be a reliable way to reinvest profits. Given the fact that Ukrainian society is a private ownership society, like the UK or Australia, the essence of such investment is rooted into effective risk-hedging mechanism. In particular, in times of economic growth housing becomes a liquid investment good, while during recessions and stagnation the housing market freezes, as had been the case in Stakhanov, prioritizing shelter function of housing over commodity and investment ones.

All mentioned combined with the global financial systems externalities that became very relevant for Ukraine since 2000s, resulted into rapid overheating of the housing market. During the period between 2001 and 2007 the average apartment price in Kyiv increased 8 times in USD equivalent, encouraging a similar increase in other cities. Ever increasing housing prices ensured an additional speculative demand for housing (Giucci, Kirchner & Voznyak, 2008). The existence of price bulb on the housing market in 2007-2008 can be indirectly proved by a number of indicators, ranging from distortion of ratio between rent and purchase price of housing to low correlation between housing prices and average income increase (Giucci et al., 2007). Also, while older houses normally had up to 2.34% of empty apartments, this indicator for the new housing peaked at 8-11%, which proves that the new housing became a flagship in housing prices speculation. Another indicators is related to mortgage finance and shows that a no less than 40% of mortgages were used for speculative purposes in 2004, while the same figure for 2006 is around 60% (Giucci et al., 2007). Rapid increase in housing prices was also supported by some minor factors, such as forming an oligopoly market in construction industry, with 7 companies dominating in Kyiv in 2005 (Giucci et al., 2007).

Such developments on the housing markets should also be viewed in relation to established network of professionals and institutions which mediates market transactions. As described by Smith, Munro & Christie (2005), normally there are three key types of market intermediaries: those who lubricate the flow of information between buyers and sellers (for example, real estate agents and property developers), those who attach a market value to property (surveyors) and those who deal with the legalities of property exchange (solicitors).

While all mentioned professional types are still quite young in Ukraine, they served a certain role in market overheating and particularly helped to form market price for apartments built in socialist times. Observations of intermediary professionals in Edinburgh conducted by Smith et al. (2005) can be used for explaining the role of estate agents in Ukraine in interpreting economic and cultural capital. For instance, the market itself is also often described as ‘an acting subject with its own will’, while everyone is just ‘following the market’ or ‘responds to market conditions’. The professional network also prevented cases of underpricing, encouraging the owners to bring prices to ‘normal’ market level, even in cases when the apartments were located in deteriorating multi dwelling buildings. The effect of uncertainty around volatile rising prices also benefited the intermediary’s commission in most cases.

Finally, one of the key features helpful for understanding Ukraine’s contemporary housing market is its reliance on USD as a key currency for property valuation and, in some cases, value transaction. After the burst of the housing price bubble in 2008, an economic downturn resulted in devaluation of hryvnya, lowering the effect of decreased housing prices. In most cases elasticity between correction of USD valuation and change in incomes or capital access condition in hryvnya is quite low, or at least slow. Following economic downturn in 2008-2009 and weak recession in early 2010s, Ukrainian economy experienced one of the severest fiscal and economic crises in its modern history in 2014-2015. In absence of housing pricing bubble experienced in 2000s, the reaction of housing prices to hryvnya devaluation and rapid real incomes decrease has been quite weak so far, due to a number of reasons. We can see several factors behind this observation, one of them being low trust in financial markets, disappearance of mortgage finance, low deposit rates in comparison to inflation rates etc. Also, we see a poverty effect, similar to one described in Eastern Ukrainian towns, where housing markets are stripped off liquidity. There are also some external factors at place, such as inflow of (IDPs) displaced persons to main cities and uncertainty caused by warfare in Eastern Ukraine and occupation of Crimea.

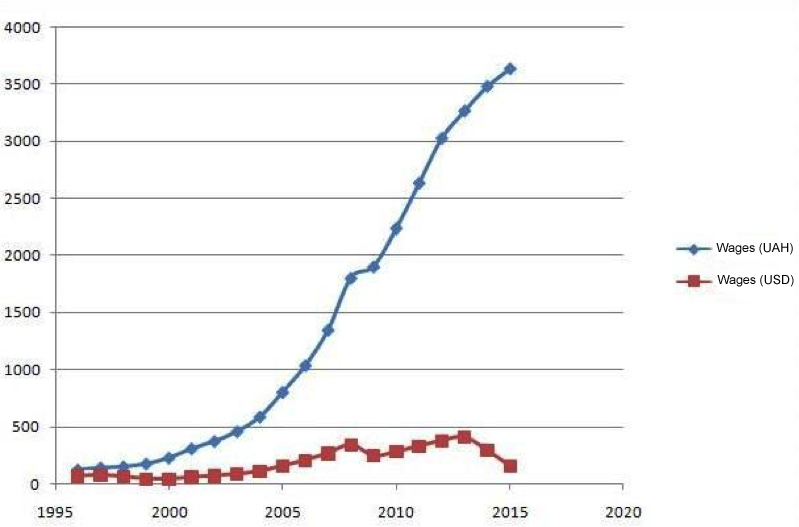

One of the most important externalities of dollarization of the housing sector is decreasing affordability of housing. This effect is most vivid if observed over time. For instance, a typical 50-meter apartment in a modernist housing on the left bank of Kyiv would costs around 10-15 thousands dollars in 1990s, which equalled 7-8 annual average incomes. In 2003 this apartment would cost around 25 thousands dollars, which would make a 12-year income equivalent based on 5 to 1 ratio between hryvnya and dollar. On the peak of pricing bubble in 2007 the price would be overheated to 120-150 thousands dollars and would be occasionally offered with a 170 thousands price tag on the market. Upon the burst of pricing bubble the market price would drop by 60%, with the new hryvnya-dollar ratio of 8 to 1. Today, such apartment would cost 50-60 thousands dollars, following slow decrease in dollar valuation over 2014 and 2015. With 25 hryvnyas exchanged for 1 USD, this means a price equivalent to 25 annual incomes. Hence, with other financial instruments temporarily out of function, dollarization makes the strongest tie of the local housing market to the global financial system, and arguably least helpful one.

While housing market dynamics in 2000s surely fits into the neoliberal paradigm observed globally, as well as the tendency towards handing responsibility over housing maintenance to private actors, other signs of neoliberal transformation in the housing market described by Sager (2011) are also emerging or yet to come. In particular, gated community has become a new market offer on the new housing market in Kyiv, providing a ‘safe exit’ for the middle class, which is experiencing increased crime rates, problems with car parking and changed demographics of the city due to inflow of internally displaced persons (IDPs). In its turn, gentrification has not yet become a buzzword in the Ukrainian context and is yet less visible in its hypsterification form, well narrated in the West. Gentrification externalities are also limited by prevalence of privatised housing in Ukrainian cities, which are less vulnerable than rentals. However, gentrifying efforts might soon become visible in cities like Kyiv, Lviv and Odesa, particularly in their historical inner towns, neglected in the Soviet times. Gentrifying efforts are also noticeable in urban renewal, yet occasional, and are less visible in a spatial dimension due to dispersed and ‘egalitarian’ nature of post-socialist cities. Given visible similarities between housing markets in countries with liberalized economies, it is well worth expecting these global trends eventually coming to Ukraine with the next wave of economic recovery.

Bibliography and references

- Andersson, R. & Turner, L. M. (2014). Segregation, gentrification, and residualisation: from public housing to market-driven housing allocation in inner city Stockholm. [Digital version]. International Journal of Housing Policy, vol. 14 nr. 1 s. 3-29.

- Baeten, G. & Listerborn, C. (2015) Renewing urban renewal in Landskrona, Sweden: pursuing displacement through housing policies, Geografiska Annaler Series B: Human Geography, vol. xx

- Бережна А.Ю. Приватизація житлового фонду і формування ринку житлово-комунальних послуг // Комунальне господарство міст, науково-технічна збірка № 87, 2009

- Букiашвілі В. О. ЖИТЛОВА ПОЛІТИКА ЯК ЕЛЕМЕНТ СОЦІАЛЬНОЇ ПОЛІТИКИ ДЕРЖАВИ: АНАЛІЗ ВІТЧИЗНЯНОГО ТА ЗАКОРДОННОГО ДОСВІДУ // ЕКОНОМІКА БУДІВНИЦТВА І МІСЬКОГО ГОСПОДАРСТВА, ТОМ 5, НОМЕР 3, 2009, с. 141-146

- Chen, L. (2008). Challenges of Governing Urban Commons: Evidence from Privatized Housing in China. Conference Paper, Governing Shared Resources: Connecting Local Experience to Global Challenges, the Twelfth Biennial Conference of the International Association for the Study of Commons.

- Florida, R. (2005). The Flight of the Creative Class, Harper Collins Publishing

- Gentile, M. (2015) The «Soviet» factor: exploring perceived housing inequalities in a midsized city in the Donbas, Ukraine. Urban Geography, 36:5, 696-720, DOI: 10.1080/02723638.2015.1012363

- Giucci, R., Kirchner, R., Voznyak, R. (2008). The Housing Construction in Ukraine: Reasons for the Current Recession and Policy Implications. German Advisory Group, Institute for Economic Research and Policy Consulting, Policy Paper Series.

- Giucci, R., Kirchner, R., Yuzephovich, I., Suchok, I. (2007). The Housing Prices in Ukraine: Trends, Analysis and Recommendations for the Economic Policy. German Advisory Group, Institute for Economic Research and Policy Consulting, Policy Paper Series.

- Glaeser, E. (2011). Triumph of the city: How our greatest invention makes us richer, smarter, greener, healthier and happier. Pan Macmillan.

- Harvey D. (2012), Rebel Cities: From the Right to the City to the Urban Revolution, Verso Books

- Kährik, A., Tammaru, T. (2010) Soviet Prefabricated Panel Housing Estates: Areas of Continued Social Mix or Decline? The Case of Tallinn. Housing Studies, 25:2, 201-219, DOI: 10.1080/02673030903561818

- Magnusson, L. & Turner, B. (2008) Municipal Housing Companies in Sweden — Social by Default, Housing, Theory and Society, 25:4, 275-296, DOI:10.1080/14036090701657397

- Marcuse, P. (2009) From critical urban theory to the right to the city, City: analysis of urban trends, culture, theory, policy, action, 13:2-3, 185-197,

- Ong, R., Parkinson, S., Searle, B. A., Smith, J. S., Wood, G. A. (2013) Channels from Housing Wealth to Consumption, Housing Studies, 28:7,1012-1036, DOI:10.1080/02673037.2013.783202

- Пинчак Л.А. Жилищный фонд Украины: состав, структура, статистика // Вестник МГСУ. 2013. No 9. С. 118–124.

- Renaud, B. M. (1996). Housing Finance in Transition Economies: The Early Years in Eastern Europe and the Former Soviet Union. Policy Research Working Paper. The World Bank, Financial Sector Development Department.

- Sager, T. (2011) Neo-liberal urban planning policies: A literature survey 1990–2010, Progress in Planning 76 (2011) 147–199

- Сердюк Т.В., Кравчук Г.В. ОСББ як чинник реформування житлово-комунального господарства // Економічний простір, № 76, 2013

- Smith, S. J. (2014) Neo-liberalism: Knowing What’s Wrong, and Putting Things Right, Housing, Theory and Society, 31:1, 25-29, DOI: 10.1080/14036096.2013.839277

- Smith, S. J. (2011). Home Price Dynamics: a Behavioural Economy? Housing, Theory and Society, 28:3, 236-261.

- Smith, S. J. (2011) Housing Economics: the Heterodox Experiment, Housing, Theory and Society, 28:3, 300-304, DOI: 10.1080/14036096.2011.599180

- Smith, S. J., Munro, M. (2008) The Microstructures of Housing Markets, Housing Studies, 23:2, 159-162, DOI: 10.1080/02673030801959361

- Smith, S. J., Munro, M., & Christie, H. (2006). Performing (housing) markets. Urban Studies, 43(1), 81-98.

- Smith, S. J., Searle, B. A. (2008). Dematerialising Money? Observations on the Flow of Wealth from Housing to Other Things, Housing Studies, 23:1, 21-43, DOI: 10.1080/02673030701731225

- Stryuk, R.J. (1996). Economic Restructuring of the Former Soviet Bloc. The Case of Housing. The Urban Institute Press, Washington DC. State

- Statistics Service of Ukraine, ukrstat.gov.ua

- The Right to Adequate Housing, Fact Sheet no. 21, UN Habitat

- Tsenkova, S., Turner, B. (2004) THE FUTURE OF SOCIAL HOUSING IN EASTERN EUROPE: REFORMS IN LATVIA AND UKRAINE, International Journal of Housing Policy, 4:2, 133-149